Posted on |

Home Buyers Versus Investors: Do You Need a Different Mindset?

The property market differs from many others, in that property isn’t always a pure “asset”. When it comes to property, people care deeply about how their home looks and how well it suits their lifestyle. It’s quite different from an investment such as, say, an endowment plan. No one cares how “nice” an endowment plan document looks; all that matters is the return.

As such, home buyers can view property in three distinct ways:

- As a pure investment asset

- A roof over your head and nothing more

- A combination of both perspectives

You can make a sound property purchase by taking on the mindset that suites one of these views.

Seeing Property As A Pure Investment Asset

A lot of people think this means seeing “only the numbers”, but that’s a half-truth. It’s more accurate to say that, if your property is purely for investment, you need to see it through the eyes of potential tenants, or future buyers.

For example, let’s say you own a car and have a family. If you run across a development like Bullion Park, you may be downright amazed – it’s freehold and it’s massive. The plot size is over 515,000 square feet, despite having just 472 units (in a new condo, you can expect twice that number of units on such a huge plot. Maybe more).

But does that make it a good investment? It’s hard to say yes, as the location is very far from any MRT station.

Tenants who are single working expatriates, couples, or students don’t really need that much space; and they’re more likely to prize accessibility over more square footage.

if your property is purely for investment, you need to see it through the eyes of potential tenants, or future buyers

Invest With Your Head or Heart?

Conversely, you may find that developments which are contrary to your instincts are actually good investments.

Would you consider Geylang area for your investment property? Probably not. Geylang conjures up all kind of negative images: brothels, loan sharks and house temples. Instinctively, Geylang goes under the radar of many investors.

But do you know the Geylang area enjoys one of the best rental yields in Singapore?

Geylang is one of the most ‘colourful’ parts of Singapore. Apart from the vices, it is known for good food and amenities. The ease of travel to CBD via MRT and proximity to Paya Lebar commercial hub helps create a big tenant pool in Geylang.

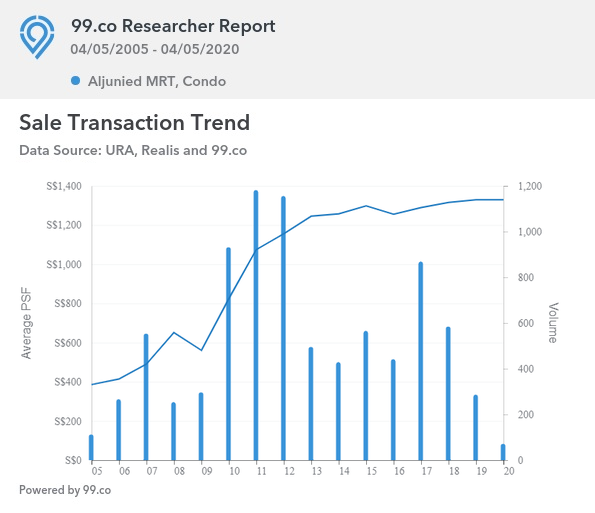

Take for example, Centra Suites at Lorong 25A, which is just across from the Aljunied MRT (3 minutes walk). I bet you have not even heard of it. You can buy a one-bedder unit at this 8-year-old freehold project for about $560,000 and fetch a rent of $1,800. That works out to a rental yield of 3.86%! And there is no shortage of tenants. You may be surprised to find quite a few angmohs in that area. They love the food, amenities and convenience.

Now you may want to stay away from Lorong 4 to 22 (even numbers) because this is the infamous red-light district and some banks may not lend you the money.

But wait a minute.

Do you know URA has rezoned this area from residential/institution to commercial/institution? This change means in future there will be a shortage of residential properties in this area which means you may stand to gain if you buy today. Would you decide with your head or your heart?

Now, Geylang may be too much for you to stomach (not because of the plethora of good food there – pun intended). I am just using this as an extreme example to illustrate my point.

See Through The Lens of Tenants

I have come across investors who would say they don’t like this or that area. That’s because they tend to see through their own lens. But when they look at the rental yields and take-up rate, then they begin to see the merits.

One of my clients went to see the show flats at Woodleigh Residences and came out impressed. They did see the potential of the upcoming Bidadari housing estate. But they decided against it because it is too near to Potong Pasir, which is an ‘opposition ward’, hence no future. I couldn’t believe my ears! I had to give them a short history lesson and reminded them the ruling party had taken over the ward since 2011!

Check Your Numbers

Besides seeing it from a tenant’s point of view, the other half of the equation is just numbers.

If you are fixated on freehold properties only, you need to consider that a freehold unit comes at around a 20 per cent premium. Your rental yield will not be attractive because of the higher outlay of capital. The fact is, leasehold projects are generally better located, making them easier to rent out. A tenant doesn’t care if the apartment he intends to rent is freehold or leasehold.

Another factor to consider is the cost of renovations and furnishings. You need to keep them to a level where you can make back the costs. Some owners treat their investment property like they are staying there by spending big bucks on ID works and high-end furnishings.

I have helped many owners to make their apartments look nice without spending a fortune. By choosing the right type of lightings, colour scheme and accessories, it goes light on their pockets without sacrificing the aesthetic.

Another strategy is to rent it out unfurnished at a relatively lower rent and then buy over the furniture from the first tenant. This is usually much cheaper, as tenants aren’t going to bring the furniture back with them overseas and need to offload it somehow.

This requires a certain degree of acumen and a good understanding of who your tenants and possible future buyers are. If you’re considering a property for investment, whatsapp me or message me so I can help you.

Another strategy is to rent it out unfurnished at a relatively lower rent and then buy over the furniture from the first tenant. This is usually much cheaper, as tenants aren’t going to bring the furniture back with them overseas and need to offload it somehow.

A Roof Over Your Head And Nothing More

This is a mindset you can take if your retirement plans, wealth growth, etc. are kept separate from your property.

In other words, you accept that your property is pure overhead, and don’t expect to make any money from it.

In most cases, this will be an approach taken by second or third-time home owners. They’ve already upgraded and intend to live out their lives in the new home. Or they have retired and are moving to a smaller place for their twilight years. It’s comparatively rarer among first time home buyers, who probably have an eye toward upgrading or right-sizing later on.

With this approach, you don’t really have to worry about capital gains, what the rental yield is, etc. You may not even be concerned about paying above the valuation, if it’s a unit that you really like (this is how a lot of “million-dollar flats” come about).

However, I should stress that the numbers still matter in one way: even if you’re not worried about returns, you should always keep it within the bounds of affordability.

Your home should not exceed your annual income by more than five to seven times (e.g. if your combined annual income is $180,000, then your home should not be more than $900,000 conservatively, and not more than $1.26 million at the most).

Also, your Income-To-Debt Ratio should be kept at 40 per cent or below, factoring the home loan (e.g. If your combined income is $15,000 a month, then your total monthly debt repayments – including your home loan – should stay at $6,000 or below).

Note that, if your property plays no role in your retirement, you should have other plans such as annuities, stock and bond investments, etc. for your later years.

However, I should stress that the numbers still matter in one way: even if you’re not worried about returns, you should always keep it within the bounds of affordability.

A Combination of Both Perspectives

In practice, most home buyers are not purely investors or home owners. Many are somewhere in between.

A typical example of this is someone who starts out with an HDB flat, but hopes to sell it at an appreciated price after the Minimum Occupancy Period (MOP). They can then use the returns to upgrade to another property.

Another example would be someone who sees their home as a retirement asset. They may plan to sell their bigger flat or condo unit at the age of 65, and then move into a smaller unit. The excess sales proceeds can then be added to their retirement fund.

These home owners cannot think like pure investors. They will be staying in their homes for many years, and possibly raising their families there, so they can’t ignore some impracticalities. Unlikely they would want to live 90 minutes away from work or trying to raise a family in a 400 sq. ft. unit.

For these home owners, they need to strike a balance. They may want to tolerate certain inconveniences, in exchange for eventual improvement in the area. For example, people buying flats in Tengah right now may not enjoy as many amenities – but there’s more room for appreciation as the area develops. If they’re staying there for the long term, they will also eventually have more amenities to enjoy.

We have seen this happens in Jurong, which was once little more than an industrial area, but has since transformed into Jurong Lake District. The same transformation is happening in Punggol, with the rise of the Punggol Digital District.

These home owners also need to be wary of buying older properties with expiring leases, such as HDB flats built in the ‘70s. While the immediate location may be convenient, they must realise that resale will be difficult. It will impact both the ability to upgrade, or to fund their retirement (properties can begin to depreciate quite noticeably after the 40-year mark).

If you’re in this position, drop me a message and I can help you to strategise your moves going forward.

Don’t Dive Into Real Estate Without a Clear Objective

You can’t really answer the question “which property is best for me” until you’ve worked out the above. The role of property in your portfolio must be understood, before you can make a reasoned decision on what is a “good buy”.

Like me on Facebook for more detail, and I’ll update you more property insights every week.

Need an opinion on your property investment plans? Want to know the value of your property? Or need help to sell or rent out your property?

Get a 1-time free 30 min Property Wealth Planning consultation. Schedule one right now by using the calendar below .

A PWP consultation includes:

- An in-depth financial affordability assessment

- Highly relevant investment insights

- A clear and customised investment road map for your real estate investment journey ahead.

Danny Han is a licensed property agent since 2005.

As a kampong (village) boy growing up in Holland Village, he has so many fond memories. He grew up with pigsty (yuk!), cemetery, swamp and communal-living (with 10 families under one roof). His childhood games were gasing (spinning top), marbles, kites, spider-fighting and tree-climbing. An open-air cinema was his source of entertainment. 7th-month Hungry Ghost wayang (Chinese opera) and getai (concert) was a once-a-year event that brought the entire village together.

What Danny is passionate about is not just about showing clients properties around Holland Village, but also enjoys sharing anecdotes and nuggets of information that are part of his growing up years.

Danny is an avid hiker and passionate foodie. He has covered most of the nature trails in Singapore, including some that are off the beaten track. Living up to his motto, “walk to eat,” he enjoys going out with his wife, a retired academician, on a food hunt across the island. He also has some foodie kakis who mix work with food. They then share their gastronomic experiences through food blogs. So do watch out, because every time he shows you a property, he will tell you what is the best food nearby!

Subscribe to receive updated practical property investment insights, property reports and good investment deals

Leave a Reply