Posted on |

8 Essentials You Should Know When Using Your CPF To Buy House

Most Singaporeans use CPF to buy house, which enables us to achieve a high rate of home ownership.

The Central Provident Fund (CPF) is a compulsory saving scheme for working Singaporeans, with contributions of 17% from employers and 20% from employees* (the rates change from age 55 on). Over time this amount, equivalent to 37% of the monthly income, earning a guaranteed 2.5 per cent interest per annum, can accumulate substantially. Part of this goes to the CPF Ordinary Account (OA) which the government allows us to use it to buy house. Though CPF is primarily for our retirement fund, using it to buying a home makes it within reach for average Singaporeans.

* Currently, the maximum amount of CPF contributions (mandatory and voluntary), known as the CPF Annual Limit, by the employee or self-employed person is capped at $37,740. As for the employers, their contributions are capped, based on a maximum Ordinary Wage (OW) Ceiling of $6,000.

While we can use CPF to buy house, there is often confusion about how exactly we can use these CPF monies. Some Singaporeans think they can pay for their whole condo with their CPF, whereas others believe that CPF can’t even be used (they may be confused because they see friends and relatives pay their HDB loan in cash).

In this article, I want to provide some clarity on how exactly your CPF can – or cannot – be used to pay for a home. It’s important to know this, as it helps you determine whether you’re in a position to upgrade, buy your first home, etc.

1. Your CPF can sometimes cover the entire down payment for HDB loans; but not for private bank loans

When taking an HDB loan, the maximum Loan-To-Value (LTV) is 90%. The other 10% of the down payment can be in any combination of cash or CPF. So, if you have sufficient CPF, you can pay your down payment entirely from CPF. In this case, there is no cash involved.

Do take note when taking an HDB loan, you would be required to use all your CPF in your OA account, with an option to keep a maximum amount of $20,000. If taking a bank loan, you can choose how much CPF to use.

For example, if you buy a flat for $500,000, the minimum down payment would be $50,000. If you have this amount in your CPF OA, you can use your CPF to cover the full down payment and even the full cost of the flat.

This, however, does not apply to private properties, including Executive Condominiums, where you can only take a bank loan. The minimum down payment is 25%. The first five per cent must always be paid in cash, while the next 20% can be in any combination of cash or CPF.

For example, say you buy a condo unit for $1 million. The minimum down payment is 25%: the first $50,000 must be paid in cash, while the next $200,000 can be in any combination of cash or CPF (so if you have $200,000 in your CPF OA, it can cover the whole remaining 20%).

2. You can use CPF to pay for stamp duties

The Buyers Stamp Duty (BSD), and Additional Buyers Stamp Duty (ABSD), can both be paid with your CPF OA. The only exception to this is the Sellers Stamp Duty (SSD), which is taken directly from your sales proceeds (the SSD only applies to people selling their private properties within three years of acquiring them).

However, note that both the BSD and ABSD are payable within 14 days of signing the Sale & Purchase Agreement or the date of acceptance of Option To Purchase, you will need to pay with cash first. Subsequently, you can apply for reimbursement from your CPF. As such, please ensure you have sufficient funds in your CPF OA account to cover the stamp duties after you’ve also used your CPF to cover your down payment (see point 1).

Otherwise, you may need to pay the difference in cash.

If you’re not sure how much to set aside, just drop me a quick note; I can walk you through how much you’ll need to save up.

3. If you’re buying landed property, you can use your CPF for the construction loan

If you’re building your own landed home, you can pay for the construction loan with your CPF. However, there are some restrictions.

First, you can only withdraw an amount up to the new valuation of the property. This limit applies to all the loans you’re using for the house (e.g. the construction loan, as well as any other existing loan to buy the property).

Second, if you already own another residential property, you must have enough CPF monies left to meet your Basic Retirement Sum (BRS). You can only use the amount in excess of your BRS for the construction loan.

4. You can pay legal fees with your CPF

The conveyancing fees when buying a property are around $2,500 to $3,000. Whether or not you can pay for this using CPF depends on the law firm; it’s possible with some firms but not with others.

So if you want to pay for this with CPF, you should be more picky about which lawyers you engage. Every bank has a given list of law firms it works with – do specify that you want a firm that can be paid via CPF.

(Mind you, that may end up being the more expensive firm; but $500+ more from CPF may be better than paying cash, if you still have renovation expenses to deal with).

For HDB loans, if you are engaging HDB lawyers, the legal fees are much lower (just a few hundred dollars). You can always use your CPF for legal fees for HDB loans.

5. There’s a limit to how much CPF you can withdraw for your flat or condo

The Withdrawal Limit (WL) is capped at 120 per cent of the Valuation Limit (VL) of your property.

The VL is the lower of the price or valuation (at the time of the transaction). So if you buy a resale condo for $1 million, with a valuation of $980,000, then your CPF withdrawal limit is $1.176 million (or 120 per cent of $980,000).

Once you hit the CPF withdrawal limit, you must pay for the rest of your housing loan with cash.

It is uncommon, but not impossible, for borrowers to hit such a high withdrawal limit. Remember that, due to the interest rate on loan, you are always paying more than the actual transacted price; so there is a chance you can hit the limit, especially if the interest rates are high.

(This is why it’s important to refinance and keep your rates low. If you’re currently paying more than 1.3 per cent per annum for a bank loan, contact me – we may be able to find you something cheaper).

6. There might be a limit to the usage of CPF for older HDB flats with leases of less than 60 years

For HDB flats or private properties that have a remaining lease of less than 20 years (before 10 May 2019 was 30 years), no CPF can be used.

If the HDB flat is left with between 30 to 59 years lease, then the age of the youngest buyer plus the remaining lease of the property must add up to 95 or more to use 100% of your CPF up to the Valuation Limit (or applicable Withdrawal Limit if higher).

Take for example of a buyer who is 40 years old, and the flat still has 56 years left (in this case, 40+56 > 95) then he can use 100% CPF.

But if the remaining lease of the flat does not cover the buyer till 95 years old, then you can only use a prorated amount of your CPF.

To know how much CPF you can use, you can check on this CPF website.

7. Things that CPF can’t be used to pay for

There are a few situations where CPF cannot be utilised:

- The purchase of non-residential property, with effect since 1 July 2006

- For those who are buying residential properties under a trust, where full cash must be used (no loan and no CPF)

- Cost of renovations

- Agent’s commission

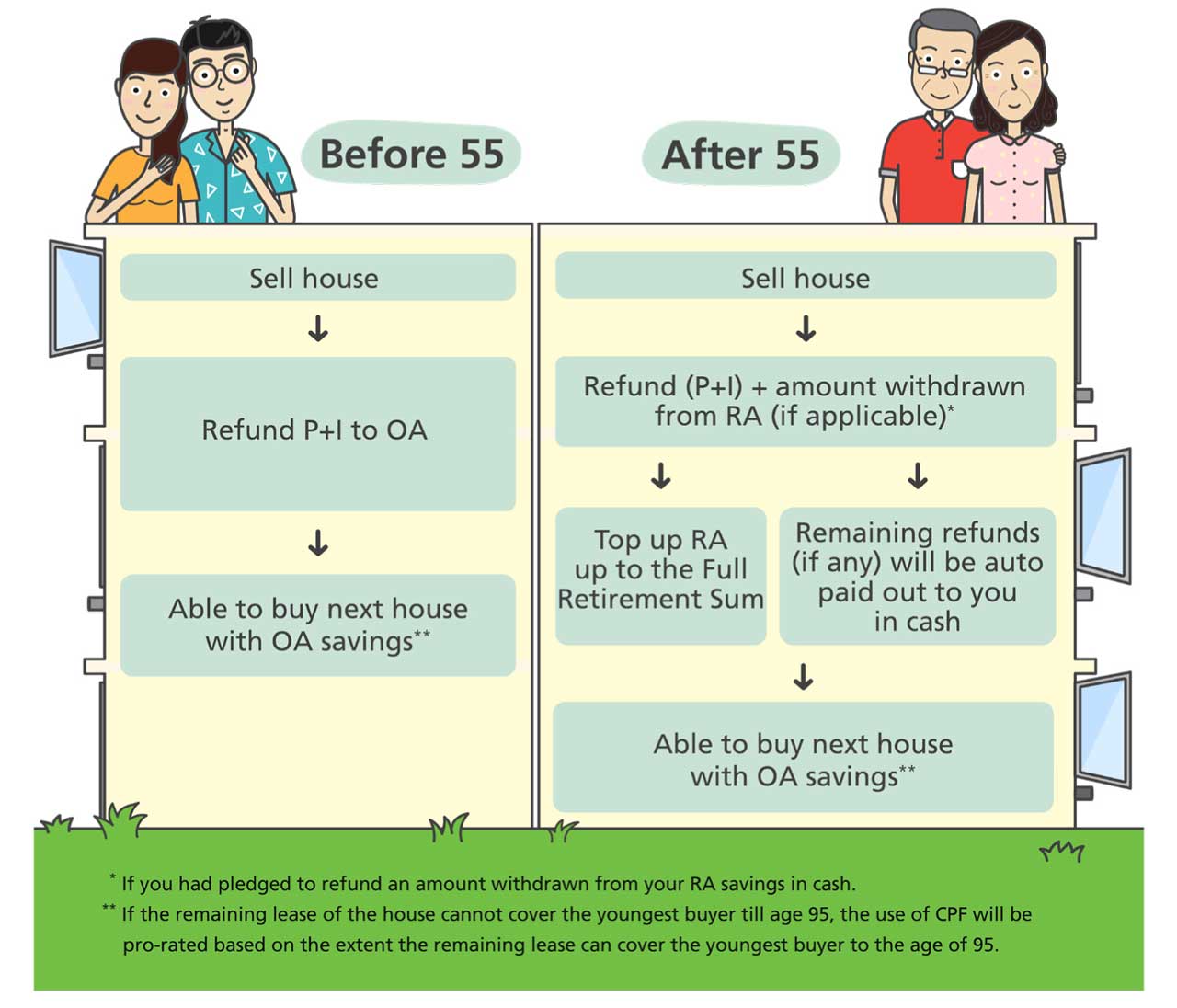

8. You must refund the CPF monies you’ve used when selling your property

This is the most important thing home owners must understand about using CPF.

When you sell your home, any amount taken from CPF – from the down payment to stamp duties to monthly home loans – must be refunded to your CPF. This is along with the interest it would have accrued (2.5 per cent per annum).

In the worst-case scenario, you might be obliged to refund more to your CPF than the entire sale proceeds; an incident known as a negative cash sale. In such an event, you don’t have to top up any difference so long as you sell the property at valuation or higher.

For example: say you sell your flat at its valuation of $500,000. However, over the years, you have used $520,000 from your CPF, in paying the home loan, down payment, stamp duties, and so forth.

You don’t have to top up the $20,000 difference (as you’re selling at valuation), but it does mean you’ll have zero cash in hand after the sale.

Now you can use your CPF again for your next home, if you’re upgrading; but a negative cash sale can be problematic if you want to upgrade to private property. Remember, you need to pay at least five per cent of the private property in cash (see point 1).

Because of this, some home buyers try to use less of their CPF, by servicing the home loan in cash (they only use their CPF for the down payment). Holding on to a property purchased with CPF for too long can result in a substantial amount of accrued interest. This is due to the effect of compound interest. The accrued interest does not stop at the point your loan is fully paid, but only until you sell your house.

Holding on to a property purchased with CPF for too long can result in a substantial amount of accrued interest. This is due to the effect of compound interest. The accrued interest does not stop at the point your loan is fully paid, but only until you sell your house.

9. You can continue to pay for your housing with CPF after 55

There’s a common misconception that, when you turn 55, your CPF OA and other accounts will be merged to form the Retirement Account (RA), so you can no longer use it to pay for your property. This is incorrect.

You can apply to reserve savings in your CPF OA before your 55th birthday. CPF will not transfer this reserved amount to your RA, and you can continue to keep using to service your home loan. You can apply to do this on the CPF website.

Also, bear in mind that if you’re still employed (even past 55), you will continue to have CPF contributions to your CPF OA, which you can still use to service your home loan.

If your RA happens to already exceed your BRS, you can also use the excess for home loan repayments.

Using your CPF, which can earn you a 2.5 per cent interest to pay for a bank loan which incurs 1.3 to 1.5 per cent interest (current rates), is not being financially prudent.

These being said, I would advise home buyers not to be reckless with their CPF usage.

CPF is not “free money”; it is still your money that you worked for. As such, be careful not to lose sight of fundamental issues such as affordability or holding power. It can be easy to forget these when CPF takes out the “sting” of paying from your pocket.

Many home buyers end up with very little or no CPF funds for their retirement. They become asset-rich but cash-poor. Do not forget CPF gives you a safe, consistent return of 2.5 per cent per annum. Using your CPF, which can earn you a 2.5 per cent interest to pay for a bank loan which incurs 1.3 to 1.5 per cent interest (current rates), is not being financially prudent.

I can offer help on how to make a reasonable home purchase, or a property wealth progression strategy, that will make the best use of your cash or CPF.

Do contact me with your questions regarding residential property in Singapore. Or make an appointment with me for a virtual meeting using the calendar below.

Danny Han has always been in the people’s business, having spent 23 years as a church pastor, five years as an insurance agent, and the last 16 years as a property consultant.

Danny has a genuine interest in people and firmly believes in personal integrity. While helping homeowners with their property needs, their interest always takes precedence over his personal gains. Hence, Danny has consistently earned his clients’ complete trust and loyalty. Many of them have become his personal friends.

Danny received his Diploma in Mechanical Engineering from Singapore Polytechnics and Bachelor of Science from Oklahoma Christian University of Science and Arts in Bible & Psychology.

Besides keeping abreast of the property market trend and constantly equipping himself to better serve his clients, Danny is a passionate foodie, a weekend cyclist, and an avid hiker.

Is It Still Worth Buying A Freehold Property For Retirement?

How Your Property Can Still Provide For Retirement In 2023 And Beyond

Subscribe to receive updated practical property investment insights, property reports and good investment deals

Leave a Reply