Posted on |

The current Covid-19 pandemic that began in Dec 2019 is growing in scale every day, with the number of infections and deaths growing exponentially worldwide.

Singapore is no exception.

Fear strikes at the chord of our heart.

Things we take for granted we can no longer do. Travel bans. Quarantines. Stay-home notices. Schools shut down. No big gathering. The list adds on as the days go by.

The disruptions to our social fabrics and the impact on our economy are unprecedented. We see the stock markets crashed. Entertainment venues such as bars, cinemas, karaoke and discos shut down. Organised tours and religious meetings suspended. All mass gatherings and events cancelled.

Social distancing has become part of our social responsibility. No handshakes. No bodily contacts (except those closest to you). 1 meter apart. ‘Zoomed’ meeting. Online training. Live-streaming. So weird. It’s not our usual way of life.

Businesses are under threat of bankruptcy. The livelihood of many people is at stake.

There are people I know who have lost their jobs, have significant pay cuts and no more bonuses.

Covid-19 is so devastating that our government has announced not one but two relief packages to the tune of almost $55 billion, or 11 per cent of our GDP.

Kudos to our government.

The relief packages will do much to help businesses and individuals through these tough times.

Tough times call for drastic measures.

When the going gets tough, the tough get going.

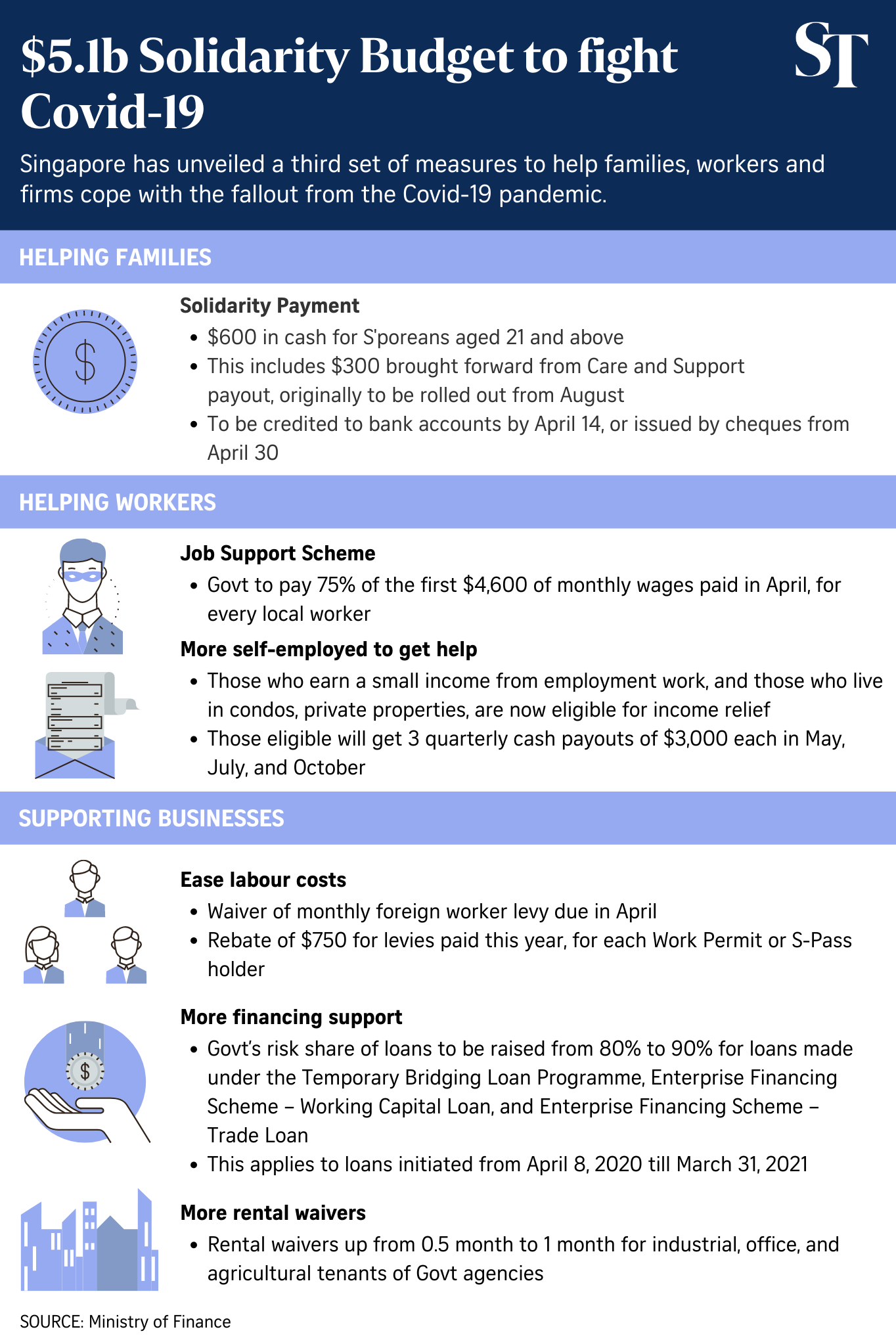

Solidarity Budget

On 6 April 2020, our Finance Minister, Mr Heng Swee Keat, announced the third relief package, dubbed the Solidarity Budget.

Another $1.1 billion will be set aside to help families, workers and businesses. This is much needed with the one-month circuit breaker measures which will see a shutdown of most workplaces and schools in Singapore from 7 April 2020 to 4 May 2020. This brings the total budget to $5.1 billion, which is unheard of in our history.

STAY SAFE AND CALM

Yes, we need to stay safe and calm.

Fear not only can paralyse us but also cause us to make hasty regrettable decisions; and irrational reaction such as fighting for toilet rolls and instant noodles at the supermarkets.

If you are a property owner, don’t panic sell.

The market will be bad for now. So it’s good to consolidate all your resources and reassess your financial position.

I am reminded of famous words of Dr Robert H. Shuller “Tough times never last, tough people do!”

The bad times will last for a while but not forever.

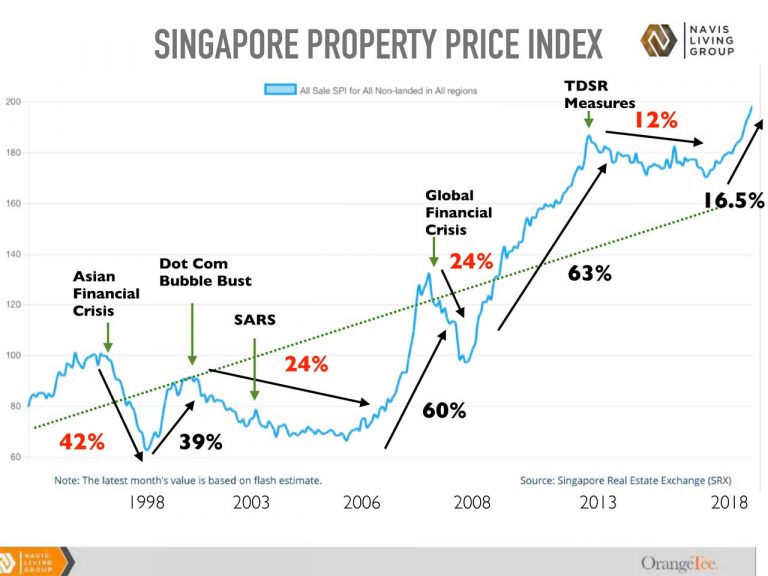

History shows us that we will recover stronger.

The crises of the past had taught us to be more prepared.

Thanks to our government for the rounds of cooling measures between 10 Feb 2010 and 6 July 2018. Today, we have more holding power which should help us weather through the Covid 19 crisis.

The government has also just announced more measures to help property owners to tide through this difficult time.

So what can you do to consolidate your financial resources without selling your property?

Refinance Your Loans

If you have an outstanding home loan and are eligible for loan refinancing, now is the time to do it.

Home loan interest rate is now at an all-time low.

In response to the fallout of the Covid 19 pandemic, on 15 March 2020, the US Federal Reserve slashed its benchmark interest rate by a full percentage point to near zero. The key rate is now zero to 0.25 per cent, matching the record low level it hit during the 2008 financial crisis which was held until December 2015.

With the protracted pandemic, interest rates will be kept low for at least the next two years. Low interest rates will help build and rebuild the battered economy.

You should take this opportunity to talk to your banker to see if you can do a refinancing.

At a time like this, banks will be more than willing to extend their helping hands, especially for those who are not able to keep up with their mortgage payments.

Let’s see how much saving we are talking about with the reduction in interest rates.

Here is the comparison chart based on $1m loan for 25 years:

If you are currently paying 2.5% for your $1m loan and refinance at 1.5%, your monthly payment would have dropped from $4,486.17 to $3,999.36. That’s a saving of $486.81 a month.

If you can secure a loan package at 1.25%, it would work out to $603.20 a month.

The myriad of loan packages may be very confusing to some.

Most people are looking now at the floating, SIBOR-pegged home loans at the moment. Rates can be as low as 1.36%, depending on which bank.

If you want more security, you can also opt for fix rate packages for about 1.68%, depending on the loan amount. The lock-in period can be 2, 3 or even 5 years.

If you need help, do let me know.

Stretch Your Loan Tenure

Apart from refinancing your loan to enjoy the low interest rates, you can also stretch your tenure by another 15 years.

Your original loan is likely up to 65 years old to get the maximum 75% Loan-To-Tenure (LTV). But for refinancing, you can stretch up to 75 years old while still enjoying 75% LTV.

By extending another 15 years, it will ease your monthly mortgage payment, thus giving you better cash flow.

Once the situation improves, you can make a partial repayment to reduce the interest costs.

Example:

Loan: $500,000

Interest: 1.4%

Current: 20 years tenure

Monthly payment: $2,389.80

If extended to 35 years, monthly payment: 1,506.55

Reducing by $883 a month can certainly help when in dire straits.

Defer Payments on Home Loans

The Monetary Authority of Singapore (MAS) has just announced homeowners who are facing financial pressure amid the Covid-19 outbreak will soon be able to apply to defer payments for their housing loan.

The payment will be deferred to 15 January 2021 for HDB loan and 4 Jan 2021 for all other loans.

There are several options.

You can choose between extending or not extending you loan tenure when your repayment resume.

If you choose to extend, for example, if you start the payment deferment in May 2020 (8 months to December 2020), you loan tenure will be extended by 8 months.

The options are deferred payments on principal payment only, or both principal and interest payments. Accrued interest only applies to the deferred principal amount and not the deferred interest payments. This is provided that mortgagor is not in arrears for more than 90 days as of 6 April 2020.

So if you choose to defer payment on both principal and interest, the principal amount will remain unchanged (for fully disbursed loan) and interest is computed on the principal amount. There is no interest charged on interest.

There will be no late fees or charges during the payment deferment period.

Some landlords may have a problem finding new tenants at this time. With no rental income, this deferment may be a life-line to home owners.

Take a Home Equity Loan

If you are affected financially and in need of funds to tide through this challenging period, you can consider taking a home equity loan if you own a private property.

A home equity loan is a secured loan using your property as collateral. Interest rate is about the lowest compared to any other kind of loans you might be eligible for. The bank will give you the money in one lump sum.

With this money, you can settle your debts that incur higher interest rates, sort out your business cash flow problem, provide for your family, pay for a major medical expense, keep up with your insurance premiums, to start a business, etc.

A savvy investor may even capitalise on the market opportunity and use the money to invest in the equity market.

Do take note TDSR is still applicable when taking a home equity loan.

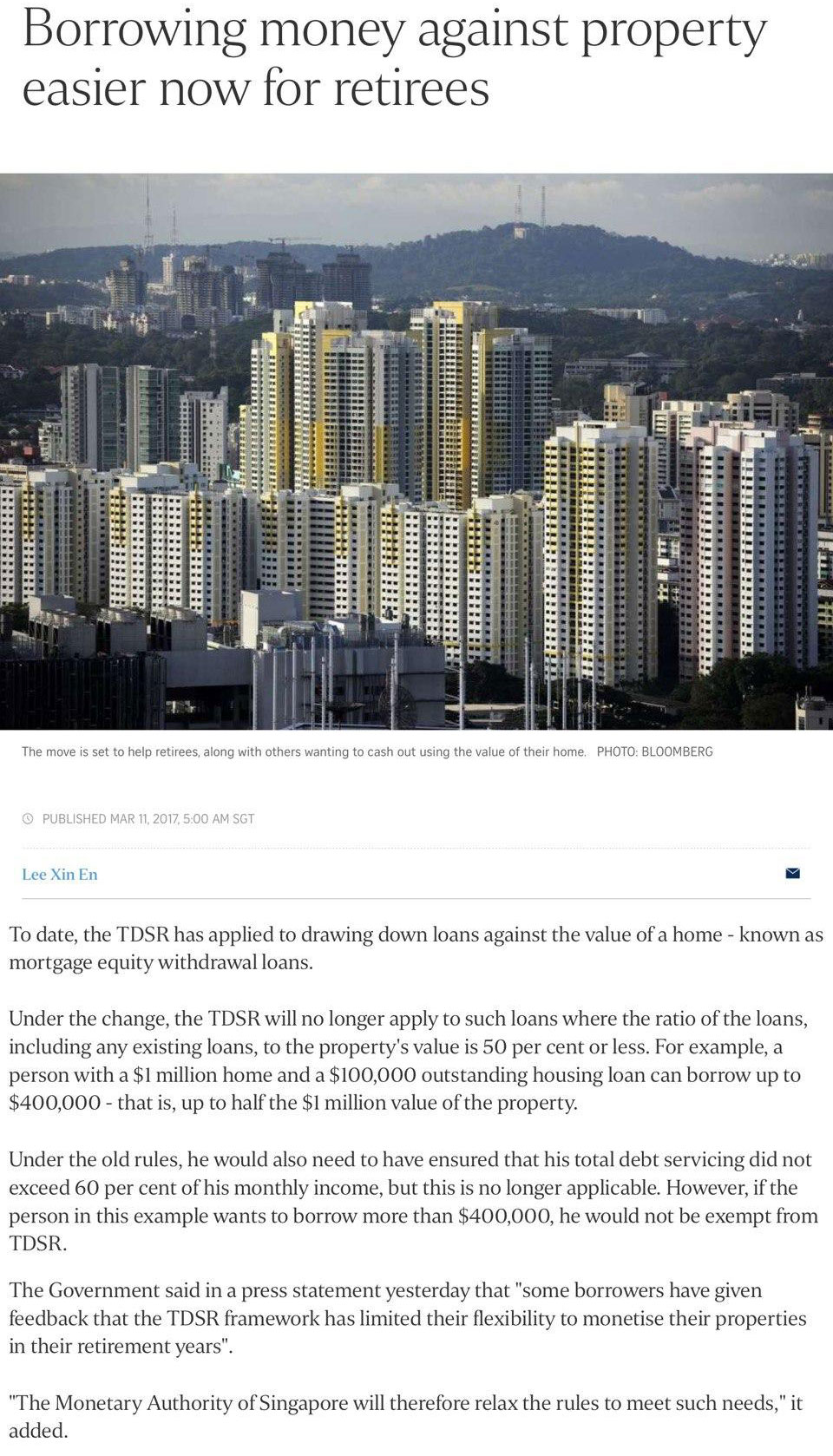

One exception is retirees. Since March 2017, the government has relaxed the rules to allow retirees to borrow against their private property. They can borrow up to 50% of their property value without subjecting to TDSR.

In a time of a severe crisis like what we are going through right now, having cash at hand can be very helpful. It could be a life-saver.

We do not know how long this Covid-19 crisis will last. It is crucial that we must have the financial resources to help us weather through this tsunami.

If you want to know more about how all these work, drop me a message or schedule a zoom meeting with me by using the calendar below.

Danny Han has always been in the people’s business, having spent 23 years as a church pastor, five years as an insurance agent, and the last 16 years as a property consultant.

Danny has a genuine interest in people and firmly believes in personal integrity. While helping homeowners with their property needs, their interest always takes precedence over his personal gains. Hence, Danny has consistently earned his clients’ complete trust and loyalty. Many of them have become his personal friends.

Danny received his Diploma in Mechanical Engineering from Singapore Polytechnics and Bachelor of Science from Oklahoma Christian University of Science and Arts in Bible & Psychology.

Besides keeping abreast of the property market trend and constantly equipping himself to better serve his clients, Danny is a passionate foodie, a weekend cyclist, and an avid hiker.

Subscribe to receive updated practical property investment insights, property reports and good investment deals

Leave a Reply