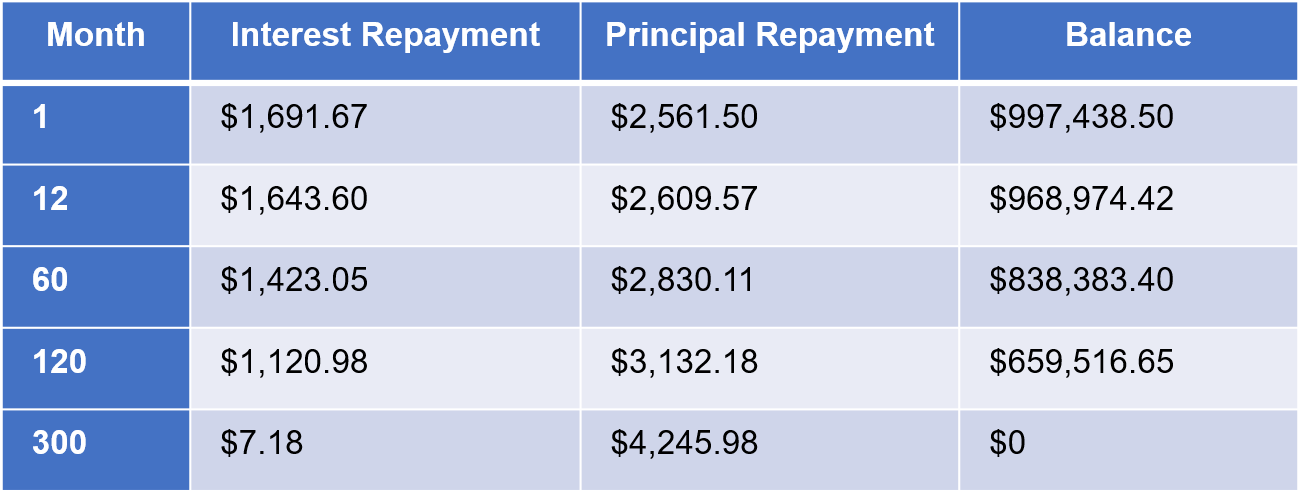

Monthly Payment: $4,094.02

Total Payments: $1,228,204.57

Total Interest Paid: $228,204.57

Slightly Lower Interest Rate Big Savings

So you can see that, with a slight “tweak” of just 0.33 percentage points, it comes to saving about $159.14 per month. If you maintain the loan at the same rate over the whole course, the difference in interest payment will amount to $47,744.57.

This extra interest is yet one more cost that eats into your gains and negatively impacts your net rental yield.

(Important to note: unlike our hypothetical example, interest rates fluctuate so you will not have the same rate throughout your entire loan tenure. I am using this to illustrate that, all things being equal, the differences in the interest rate can impact your bottom line. Hence, it sometimes justifies accepting the lock-in clause for a lower rate).

For Singaporeans who don’t intend to refinance, especially when the current interest rate is so low, a lock-in period of two or three years is not a key restraint. In fact, most home loans are cheap for three years and then jump on the fourth. So you would be getting a lower rate, with no real penalty.

Leave a Reply