Posted on |

5 Blind Spots When Selling Your HDB Flat

You might be thinking about selling your HDB flat.

- 5 year Minimum Occupation Period (MOP) is up. Time to cash out your BTO flat. Perhaps to upgrade to private property.

- You want to grow your property portfolio through sell one buy two.

- You and your wife are now empty-nesters, and you are considering to downgrade to a smaller HDB flat for retirement. Housekeeping a big house can be very tiring as age catches up. Climbing up and down the stairs in your EM flat is increasingly challenging for your knees.

- Your family size has grown, and you need a bigger house. Having now three kids, each of them needs a room to themselves (these days children are very privileged).

As you are thinking about selling your HDB flat, do watch out for these five blind spots!😎😵🧐.

Blind Spot #1: RETIREMENT SUM

Most people buy and pay for their HDB flats using CPF.

Whatever amount of CPF you have used for the house, you need to return to your CPF account, plus accrued interest. After factoring in the CPF refund, you are counting on the cash proceeds and CPF you can plan for your retirement and next purchase.

BUT….

you have already passed the magical age of 55 years old (time passes by so fast that you don’t even realise it!👴🧓). And you do not have much money in your CPF now. After all, you had used most of your CPF to fund the flat.

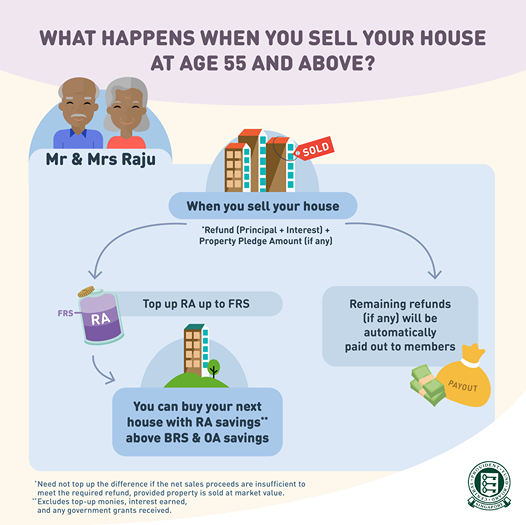

Top Up Your Full Retirement Sum

After selling your HDB flat and having refunded the CPF used plus accrued interest, you will need to top up your Full Retirement Sum FRS (previously known as Minimum Sum) for your Retirement Account (RA). The FRS depends on which year you turned 55 (see chart below).

You can only draw out the amount over your FRS. For your next purchase, you can use the amount in excess of your Basic Retirement Sum (BRS) which is 50% of your FRS.

So you have to do your sum correctly to ensure you have enough CPF (if you are counting on it) and cash for your next purchase.

Blind Spot #2: CPF ACCRUED INTEREST

Let’s suppose you bought your HDB flat 30 years ago. Just a few years ago you had fully paid up all outstanding loan. The value of your flat has appreciated. You have hope to upgrade to private property.

So you are expecting a healthy amount of cash proceeds from selling your HDB flat.

You need the cash balance to pay for the downpayment for the new condominium you have always aspired to own.

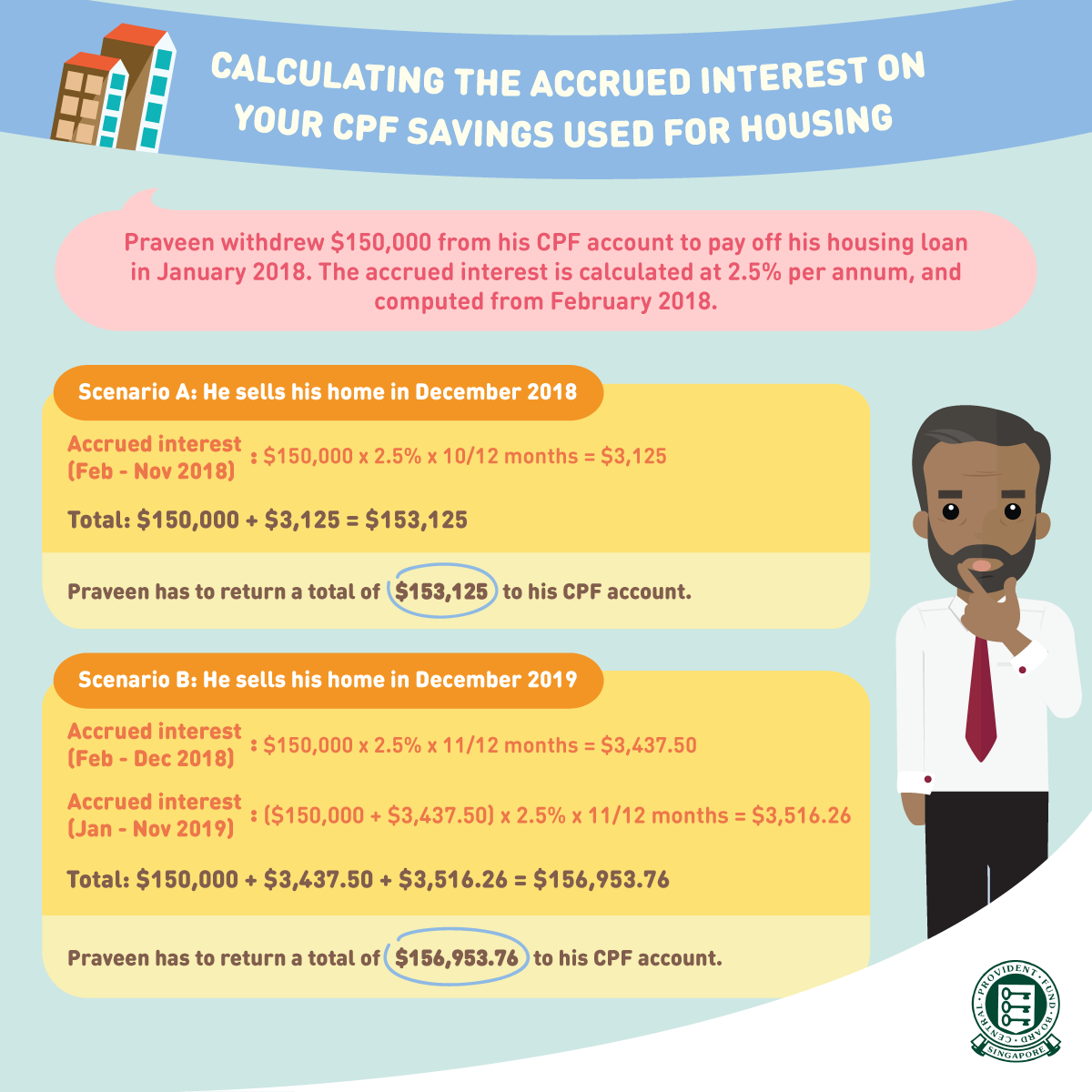

But to your horror, you find out you need to refund a massive amount of money to CPF. What you do not expect is the amount of accrued interests.

In the first place, why is there accrued interest?

Accrued interest is the interest amount that you would have earned if your CPF savings had not been withdrawn for housing. The interest is computed on the CPF principal amount withdrawn for housing on a monthly basis (at the current CPF Ordinary Account interest rate) and compounded yearly. (Source CPF)

Accrued Interest Doesn’t Remain the Same Even You Have Paid Up Your Loan

You have thought since you had already cleared your HDB loan a few years ago, the CPF refund won’t be so much. But the accrued interest gets more with each passing year, whether there is any outstanding loan or not.

So the key is, the longer you keep your flat, the more the accrued interest you need to pay back, and the lesser the cash proceeds.

In the illustration above given by CPF, Praveen only uses $150,000 of his CPF to pay for his housing loan. In Scenario B, his accrued interest is $3,437.50 for the first 11 months. In the second 11 months, the accrued interest is $3,516.26. Why is it higher? It is because the interest is compounded.

Power of Compound Interest

Albert Einstein famously said, “Compound interest is the 8th wonder of the world. He who understands it, earns it; he who doesn’t, pays it.”

Just to illustrate the power of compound interest, take a look at the table above. Suppose you have used a one-time amount of $100,000 CPF money for the purchase of your flat which would have earned you 2.5% interest per annum, after 10 years, the total interest is $28,008.45.

If you sell your flat after 20 years, your total accrued interest would be $63,861.64.

And after 30 years, the accrued interest is a massive $109,756.76, which is more than your base amount of $100,000!

As a real life example, one of my clients had used $69,802.17 of her CPF for her flat, and was fully paid up years ago, her accrued interest was $31,193.11. That was a whopping 44.7% of the amount she had used!😣😖😤

Watch out for this blind spot!

Blind Spot #3: NEGATIVE SALE

Two years ago, I helped a client to sell his HDB flat which he bought for in 2010 for $400,000 using 100% CPF.

When he sold his flat, the value had dropped to $380,000. He ended up with no cash from the sales proceeds because all the money from the sales had to go back to CPF. There was a shortfall because he was supposed to refund $400,000 plus accrued interest.

HDB even clawed back the $5,000 cash from the deposit the buyer paid.

Luckily he didn’t have to top up the shortfall because he sold the flat at market value.

If you have bought a resale flat between 2012 and 2013, there is a good chance you might end up with a negative sale when selling your flat, especially if you had used a fair bit of CPF.

With no cash from the sales proceeds, it may throw you off as you plan for your next housing. Or you may not have the money you need for your retirement or a planned vacation.😥😐

Blind Spot #4: 2ND HDB CONCESSIONARY HOUSING LOAN

If you are upgrading or downgrading to another HDB flat, chances are, you will be like most people, plan on taking a second HDB concessionary loan.

There are good reasons to take HDB loan instead of bank loan despite the higher interest rate. One main reason is you can borrow up to 90% of the value of the flat. You can then use CPF to pay the remaining 10%. In this way, you don’t need to touch your cash reserves.

Singaporeans are entitled to two times of concessionary loan. The interest rate is pegged at 0.1% above the CPF rate. Currently, the concessionary interest rate is 2.6%.

Without this concession, you will need to pay the current HDB market rate of 3.16%.

Cap on the Amount of Cash You Can Keep

To enjoy the HDB concessionary rate the second time, there is a catch.

The catch is the limit to the amount of cash you can keep from the sales proceeds.

“Generally, flat buyers can keep the greater of $25,000 or 50% of the cash proceeds (including the cash deposit received), and HDB will take into account the remaining part of the cash proceeds when determining the quantum of the second HDB concessionary housing loan.” (Source: HDB)

Different Scenarios

How does this work?

Scenario 1: If your cash proceeds amount to $25,000 or less, you can keep the full amount.

Scenario 2: If your cash proceeds work out to $40,000, you can keep only $25,000 since 50% of $40,000 is only $20,000.

Scenario 3: If your cash proceeds totaled up to $100,000, 50% is $50,000. That means you can keep $50,000 since it is greater than $25,000. The other $50,000 must be used to pay for the next flat.

Again, the lesser than expected cash proceeds may affect your plans. For example, you need it for your renovations for your next flat.

Blind Spot #5: RESALE LEVY

Like every Singaporeans, you want to enjoy your privilege as a citizen to buy a flat directly from HDB at a subsidised price.

Or if you buy from the open market, you can enjoy the housing grant given to first-timers.

Both of these situations are subject to income ceiling.

Then you decide to apply for another BTO flat. Or buy a newly launched EC.

What you might have overlooked is the need to pay resale levy in this case when selling your HDB flat. The amount depends on the type of subsidised flat you own (see chart).

When is Resale Levy Not Applicable

Resale levy is not applicable if you are buying any of these:

- Design, Build and Sell Scheme (DBSS) flat from a developer

- EC from a developer, where the land sale was launched before 9 December 2013

- HDB resale flat

- Private residential property

A client of mine was the first owner of a EM flat. She then decided to downgrade to a studio flat. Her resale levy was a whopping $50,000! That ate up into a big chunk of her retirement fund! Ouch!🤮😰

These five blind spots are by no means exhaustive. If you are thinking about selling your flat, it is worth the while to engage an experienced agent to avoid some potential costly pitfalls.

You can Whatsapp me to get an idea of your home’s value; we can also work out a way to best use your home as a path to wealth and a happier retirement.

Like me on Facebook, and I’ll update you on future articles.

Need an opinion on your property investment plans? Want to know the value of your property? Or need help to sell or rent out your property?

Get a 1-time free 30 min Property Wealth Planning consultation. Schedule one right now by using the calendar below .

A PWP consultation includes:

- An in-depth financial affordability assessment

- Highly relevant investment insights

- A clear and customised investment road map for your real estate investment journey ahead.

Danny Han has always been in the people’s business, having spent 23 years as a church pastor, five years as an insurance agent, and the last 16 years as a property consultant.

Danny has a genuine interest in people and firmly believes in personal integrity. While helping homeowners with their property needs, their interest always takes precedence over his personal gains. Hence, Danny has consistently earned his clients’ complete trust and loyalty. Many of them have become his personal friends.

Danny received his Diploma in Mechanical Engineering from Singapore Polytechnics and Bachelor of Science from Oklahoma Christian University of Science and Arts in Bible & Psychology.

Besides keeping abreast of the property market trend and constantly equipping himself to better serve his clients, Danny is a passionate foodie, a weekend cyclist, and an avid hiker.

Subscribe to receive updated practical property investment insights, property reports and good investment deals

Leave a Reply