Posted on |

Timeline Planning for Upgrading from HDB to Private Condo

To upgrade from an HDB to a private condo is one step away from fulfilling the Singaporean dream. This upward mobility is a natural progression for an affluent nation like ours, where many aspire to enjoy not just homeownership but a lifestyle.

Have you taken the first step by assessing your financial status?

So with the financial planning done for upgrading from HDB to private condo, what’s next?

The next step is to do a timeline planning for upgrading from HDB to private condo.

(Please read: “Financial Guide to Upgrading from HDB to Private Condo”).

Before you start shopping around for your dreamed condo, you have to consider these options:

- Keep your HDB flat and buy condo

- Buy condo first then sell your HDB flat

- Sell your HDB flat first then buy condo

- Sell your HDB flat and buy condo concurrently

The other question is, should you buy resale or new launch? (Read my article on “Investment Property: 6 Reasons Why New Launch is Better Than Resale”)

Option 1: Keep HDB Flat and Buy Condo

- Own two properties with one for rental income (can be HDB or condo)

- No need to worry about timeline since there is no need to move out of your current HDB flat

- Have to pay 20% ABSD

- Can’t do decoupling for HDB flat

- HDB flat likely to depreciate over time

- Need high capital outlay for condo purchase

- If you have an outstanding HDB loan, you can only take 45% loan for condo purchase

If you have fulfilled your five years Minimum Occupation Period (MOP), you are allowed to keep your HDB flat and buy a condo. You can choose to continue staying in your HDB flat or move into your new condo.

Maybe you are thinking, why not keep your HDB and rent it out since the rental yield is very attractive? Then with the rental income, you can use it to finance your new purchase. Sounds very logical?

But do take a step back and consider the disadvantages.

Firstly, since the new purchase will be your second property (HDB doesn’t allow part-sale or commonly known as ‘decoupling’), you would need to pay an Additional Buyer Stamp Duty (ABSD) of 20%. Yes, no kidding! 20% is a lot of money.

Many people loathe the thought of throwing away this considerable sum of money.

If you were to buy a $1.2 million condo, a 20% ABSD amounts to $240,000. Suppose you rent out your flat at $3,500 a month or $42,000 a year, the $240,000 ABSD will set you back by 5.71 years in rent.

Oh no! It’s like going through another round of M.O.P.!

Your HDB flat will likely depreciate over time, especially for older flats with the concern over tenure decay.

Not only that, but you would also need to fully clear your HDB loan to enjoy the maximum 75% loan for your condo purchase. Otherwise, you can only borrow 45%.

HDB prices might have gone up since Covid-19, the trend may not last indefinitely. The spike in prices is the mainly due to a shortage of supplies on the market caused by the pandemic. BTO flats were delayed. Cost of labour and materials went up. More buyers turned to resale flats instead of waiting for BTO flats. Furthermore, with more CPF grants, it makes resale flats more attractive than before.

To meet this shortage, HDB is ramping up more BTO flats to meet the demand. Construction time is also now shortened. Hence, we may see the current shortage situation stabilised over time.

On the other hand, private property prices have appreciated more than HDB prices in the last 10 years (see chart above).

Hence, to buy a $1.2 million condo without selling your HDB flat, you would need at least 25% (5% down + 20% ABSD) in cash, which is $300,000.

And if you don’t have enough CPF to cover the other 20% plus $38,600 Buyer Stamp Duty (BSD), you would need another $278,600 of cash.

This upfront capital outlay makes it out of reach for many people.

Option 2: Buy Condo First Then Sell HDB

- Can carefully choose the right property

- Have the time to renovate and move into the new house

- Has to pay ABSD first but can claim back if new purchase is a matrimonial home (i.e. buy under husband and wife’s names) and sell the HDB flat within six months. This upfront financial commitment may present some cashflow problem.

- If you still have outstanding HDB loan, the maximum amount you can borrow is 45%, so you would need more capital outlay to buy a condo.

If you choose to buy condo first then sell your HDB, the disadvantages are quite similar to the first option, namely there will be issues with ABSD and loan. The initial capital outlay is very high.

However, though you have to pay the ABSD first, if you can sell your HDB flat within six months, you can apply for remission and get back the money. This remission only applies to the matrimonial home; that is, the property must be in both husband and wife’s names. For singles, widows/widowers and divorcees, there is no remission.

On a positive note, with this option, you can shop around for your dream home without any pressure. In this way, you are more likely to make a good decision.

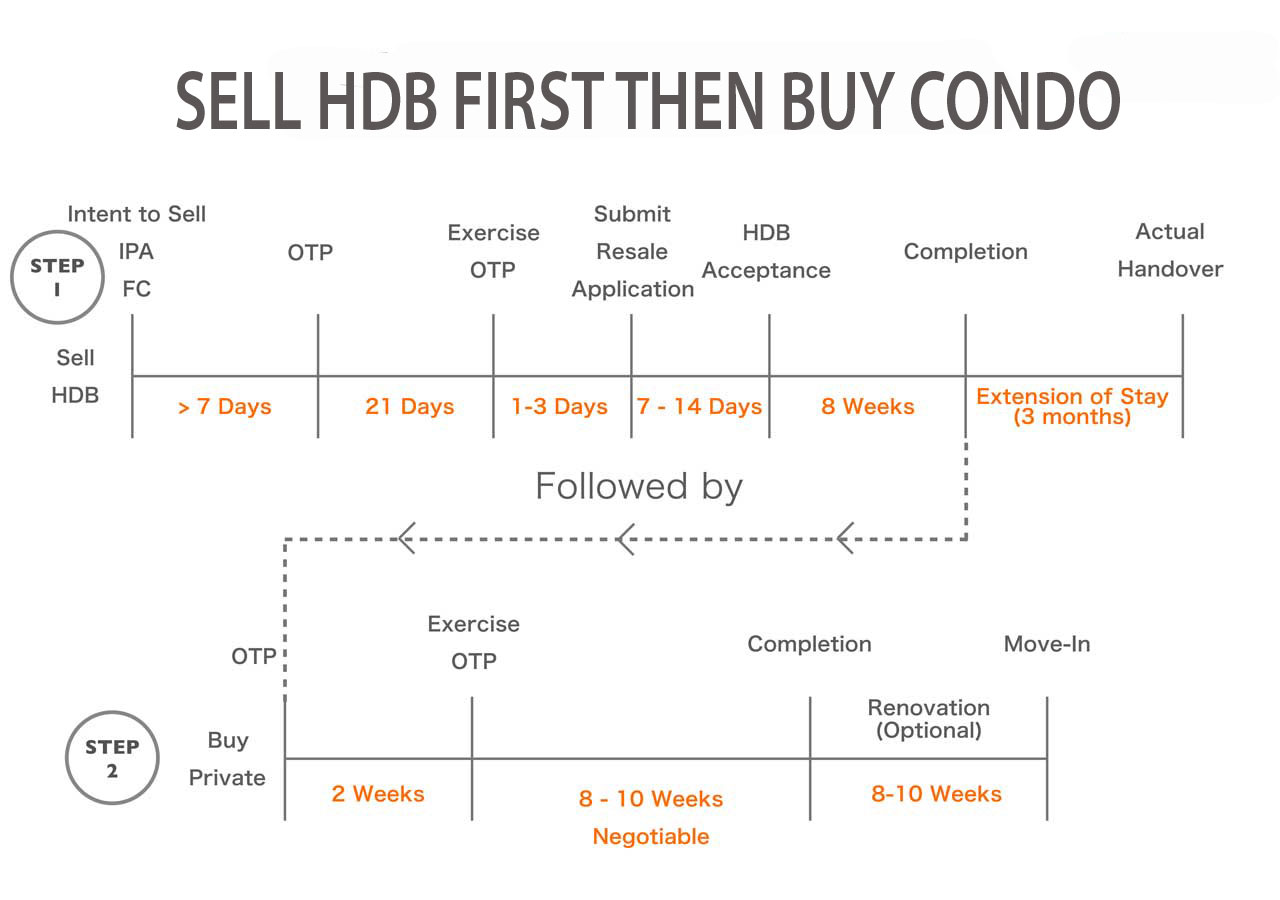

Option 3: Sell HDB First Then Buy Condo

- No ABSD

- Can take time to find the ideal home

- No cash flow problem

- Sell HDB at a higher price NOW than a lower price LATER

- May need to find temporary accommodation after selling your flat eg. renting

- Cost of renting a place during the interim period

The biggest advantage of selling your HDB first is not having to pay ABSD, thus easing your cash commitment. Plus, with the sales proceeds from the HDB, it will reduce your cash flow when paying for the new purchase.

If you are selling your HDB flat to buy a new condo launch, you will need to find a temporary place to stay before T.O.P.

If you have to rent during the interim period, you will need to factor in the cost of rental. With current rental at an all time high, this could be a deterrent. It would be ideal if you can stay short-term with your parents or relatives.

It’s also wise to book a new condo during launch to enjoy early bird discounts and first mover advantage. So, selling your flat first will free you from the time constraint to buy a new condo.

Some do not like the idea of having to move twice and having to rent for say, two to three years before the new place is ready.

However, it is wise to book a new condo during launch to enjoy early bird discounts and first mover advantage. So, selling your flat first will free you from the time constraint to buy a new condo.

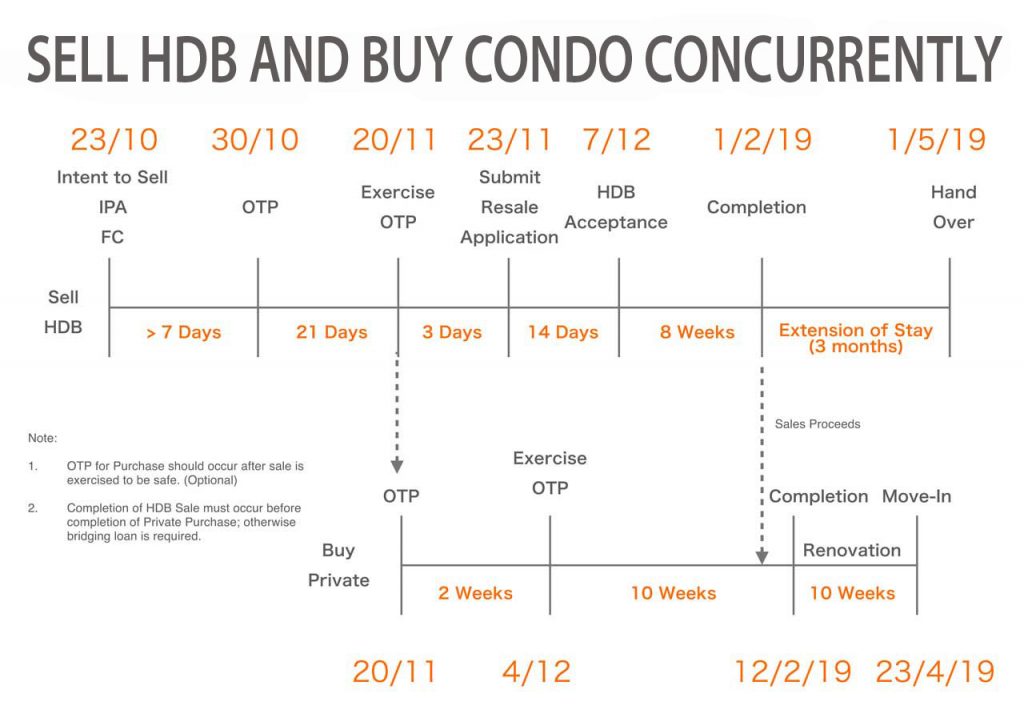

Option 4: Sell Your HDB Flat And Buy A Condo Concurrently

- Time to find the ideal house

- Have time to renovate

- No need to arrange for temporary accommodation

- No ABSD if planned well

- Need to have sufficient cash to pay 5% cash and Buyer Stamp Duty

- Need proper timeline planning

- The buyer for your flat may not be willing to grant you an extension of stay

The idea for this course of action is to time the selling and buying such that:

- After the buyer for your HDB flat exercises his option to purchase, you can commit to your condo purchase. Theoretically, your buyer can’t back up after exercising OTP, so you are quite safe. But to be even safer, you wait till HDB acceptance after submitting the resale application. This is because there are cases when the buyer can’t go ahead with the purchase for various reasons.

- You exercise your OTP after your buyer to avoid having to pay ABSD

- Completion of your HDB sale comes before the completion of your purchase so that the sales proceeds can help to pay for the purchase. If this is not possible, you would need to apply for a bridging loan. If you need to use the CPF from the sales proceeds for the purchase, do note it takes about two weeks before the money is credited into your CPF account.

Since the HDB completion occurs before the completion of your private condo, you need your buyer to grant you an extension of stay. Again, you need to express this intention up front before you accept his offer.

To facilitate a seamless move from your HDB flat to your condo takes careful planning to execute, so be sure you seek the help of an experienced agent.

Are you still confused? Are you lost in the jungle? Still not sure which option to take? Fret not because I am here to help you.

Everyone’s situation is different. Contact me for a non-obligatory discussion and I can help you devise a bespoke plan to realise your upgrading goal from HDB to private condo.

Go to my facebook page and like my page so that you can be notified of my upcoming article on how to choose the right condo.

Need an opinion on your property investment plans? Want to know the value of your property? Or need help to sell or rent out your property?

Get a 1-time free 30 min Property Wealth Planning consultation. Schedule one right now by using the calendar below .

A PWP consultation includes:

- An in-depth financial affordability assessment

- Highly relevant investment insights

- A clear and customised investment road map for your real estate investment journey ahead.

Danny Han has always been in the people’s business, having spent 23 years as a church pastor, five years as an insurance agent, and the last 16 years as a property consultant.

Danny has a genuine interest in people and firmly believes in personal integrity. While helping homeowners with their property needs, their interest always takes precedence over his personal gains. Hence, Danny has consistently earned his clients’ complete trust and loyalty. Many of them have become his personal friends.

Danny received his Diploma in Mechanical Engineering from Singapore Polytechnics and Bachelor of Science from Oklahoma Christian University of Science and Arts in Bible & Psychology.

Besides keeping abreast of the property market trend and constantly equipping himself to better serve his clients, Danny is a passionate foodie, a weekend cyclist, and an avid hiker.

Subscribe to receive updated practical property investment insights, property reports and good investment deals

Leave a Reply