Posted on |

How Will The Latest Round of Cooling Measures Impact Our Property Market?

The government announced the latest round of cooling measures on the late evening of December 15, 2021.

Did you see it coming?

The writings were actually on the walls. Property prices across the board have gone up fast and furious despite the pandemic.

The private property prices see a six straight quarters growth. As of November 2021, the overall price index has gone up by 9.3% year-on-year.

Developers sold 12,467 new homes for the first 11 months of 2021, more than the 9,982 new homes sold in the whole of last year. New home inventory has dropped to an all-time low of about 15,000 units, which has sparked a new wave of en bloc fever. We saw some recent Government Land Sales (GLS) and en bloc sales setting new benchmarks.

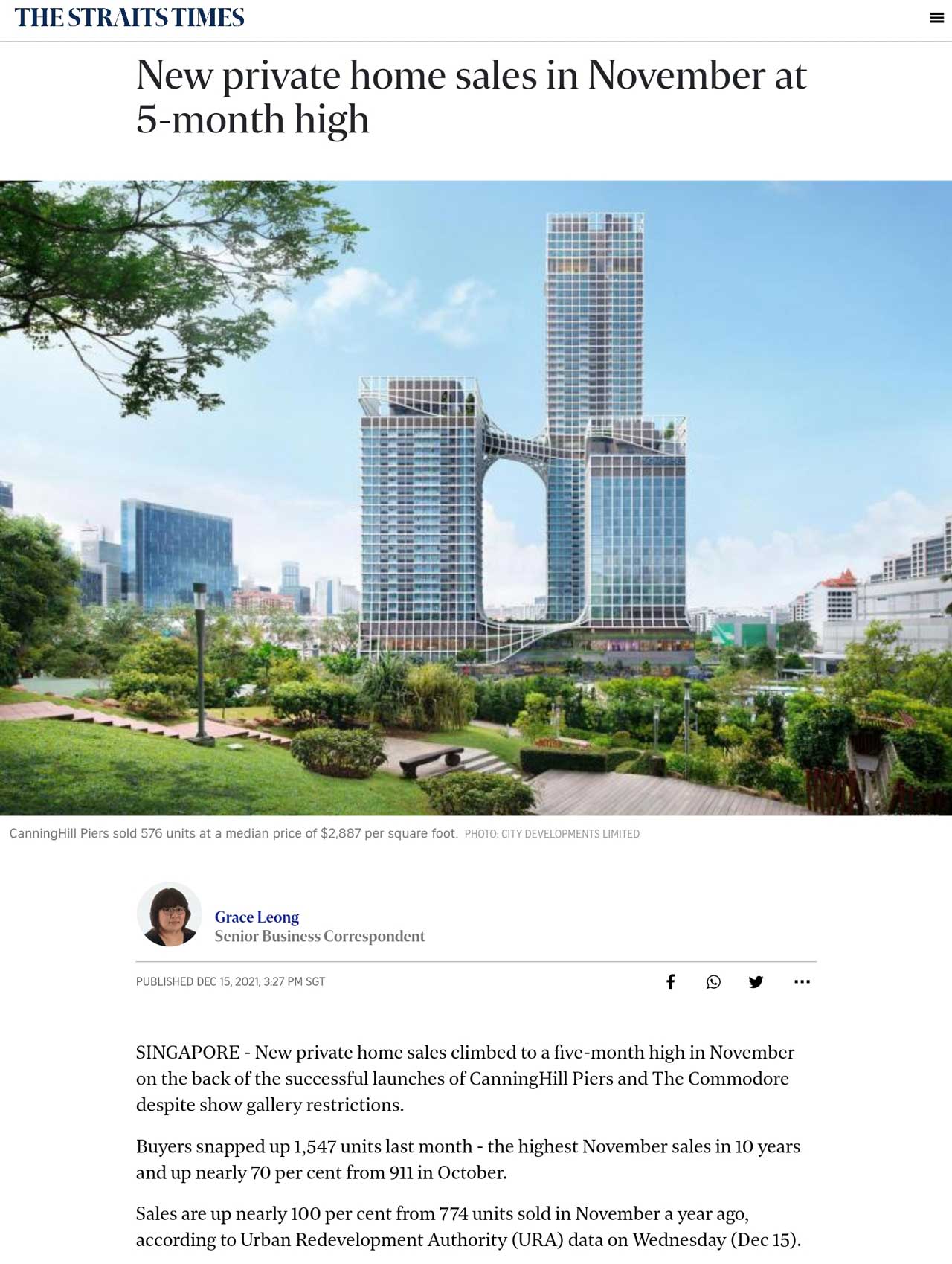

In November 2021, the property market registered 1,547 units sold, largely fueled by CanningHill Piers which sold 576 units at a median price of $2,887 per sq ft (psf). A Singaporean businessman bought the sole penthouse on the 48th floor for $48 million or $5,360 psf.

The luxury market in Core Central Region (CCR) is very buoyant, with the price level hitting more than $5,000psf. Foreigners have helped drive the demand for this upmarket segment. For example, in Park Nova at Tomlison Road, foreigner ownership stands at almost 90%.

Demand for landed property is robust, with a record number of landed homes sold and prices increasing by 9% for the first three quarters in 2021.

As for the HDB resale market, we saw a reversal of fortune since Q3 2019 after moving downhill from its last peak in Q2 2013.

HDB resale prices have gone up by 8.9% for the first three quarters of 2021, and cash-over-valuation (COV) is now commonplace.

Recently, I sold a 5-year-old 3-room flat in Yishun with a whopping $70,000 COV!

As of October 31, 192 resale flats transacted at above $1 million in 2021, compared to 82 in 2020.

In the light of such a bullish market, the government saw fit to introduce the latest round of cooling measures.

What are these measures, and what are their possible impact?

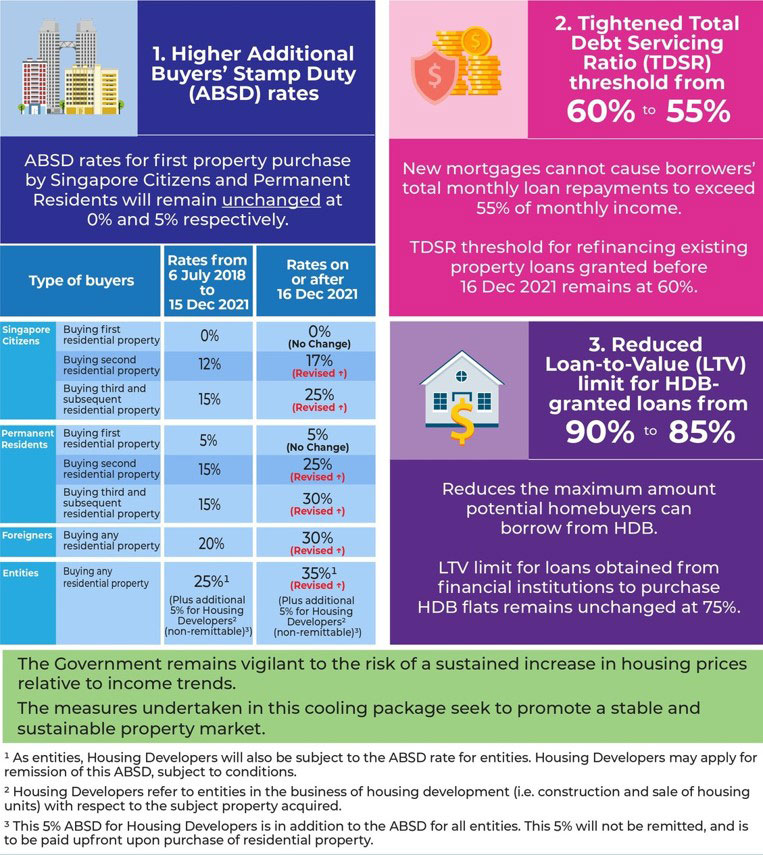

Higher Additional Buyer Stamp Duty (ABSD)

ABSD Does Not Affect First-Time Singapore and PR Buyers for Their First Property

At a glance, there is minimal impact on first-timer Singaporean buyers in terms of ABSD.

Every Singaporean will still enjoy their zero ABSD privilege when buying their first property. However, if they were to buy their second and third property, the ABSD incurred would be a hefty 17% and 25%, respectively.

Singapore PR buying their first property remains unchanged in their ABSD payable, which is 5%. But subsequent purchases will be slapped with a substantial 17% to 25% ABSD.

Foreigners, Companies and Developers Will Have To Pay Higher Rates

On the other hand, foreigners will have to pay a hefty 30%, up from 20%.

Developers will also have to pay 35% ABSD if they fail to sell every single unit of the condo development five years from acquiring the land.

Change In Total Debt Servicing Ratio (TDSR)

The government also tightens the Total Debt Servicing Ratio (TSDR) by reducing it from 60% to 55%. This means the borrower’s monthly mortgage payment cannot exceed 55% (include all other commitments, such as car loans and credit card instalment payments) of the monthly income.

Apparently, the government wants to ensure that home buyers remain prudent and do no buy beyond their means.

A lower TDSR means lower loan eligibility for home buyers.

But what is the impact of a 5% reduction?

An Example

Take, for example, a 30-year-old couple with a total monthly income of $12,000. With the change in TDSR, they can borrow up to $1.47m, down from the previous $1.6m. So with this $130,000 difference, unless they can fork out more cash, they will have to settle for a lower-price property.

Loan-To-Value (LTV) For HDB Loans Reduced From 90% to 85%

This change will only affect HDB buyers who are taking HDB loans. As for those taking bank loans, the LTV remains at 75%.

If an HDB buyer has sufficient CPF funds in the Ordinary Account (OA) account, he can use it to pay for the 15% downpayment without forking out any cash, assuming he can borrow up to 85% of the value of the flat.

For example, if the valuation of an HDB flat is $500,000, it means the buyer can take a maximum HDB loan of $425,000 instead of $450,000. The 15% downpayment, which is $75,000, can be paid entirely with CPF. With the generous housing grant of up to $50,000 for first-timers and another $20,000 for proximity grant, they would almost cover the 15% downpayment required. If they are eligible for Enhanced Housing Grant (EHG), they even have enough CPF to spare.

Will this stop HDB buyers from buying an HDB flat? Probably not.

Most average Singaporeans will still purchase an HDB flat to provide a roof over their heads.

For some HDB buyers, their affordability might be affected to some extent, especially for young couples or low-income families who don’t have much CPF or cash reserves. They will then need to lower their expectations by paying a cheaper resale flat that is older or in lesser premium locations.

Will We See A Major Correction In Property Prices?

Upon hearing the announcement of the cooling measures, one of my clients shouted “Hallelujah!” because he expected property prices to come down.

Will that happen?

It is very likely for the next couple of months, home buyers will wait on the sidelines to let the dust settle and see how the market moves. But after a very short hiatus, the market will likely pick up again. We have seen this same thing happen in the past.

History of Cooling Measures

Not long after the 2008 Global Financial Crisis, when the property market started to pick up strongly, our government introduced the first round of cooling measures in 2010. Despite rounds of cooling measures, they did not stop the tide of home buyers and property investors.

This latest round would have been the 11th round of cooling measures.

How would they impact the property market?

Impact of TDSR in the Past

The last peak was in 2013, which came to a screeching halt after the government Total Debt Servicing Ratio (TDSR) for the first time.

At the new 55% TDSR, it means your total debt monthly payment must not be more than 55% of your monthly income, based on an interest rate of 3.5% (not the actual borrowing rate).

TDSR, together with a lower Loan-To Value (LTV), are in place to curb speculations. Before its introduction, speculators borrowed vast sums of money to leverage and flipped for profits.

So will reducing the TDSR from 60% to 55% affect the market?

Singaporeans have long gotten used to TDSR, unlike in 2013. Psychologically, this round did not come as a rude shock to us.

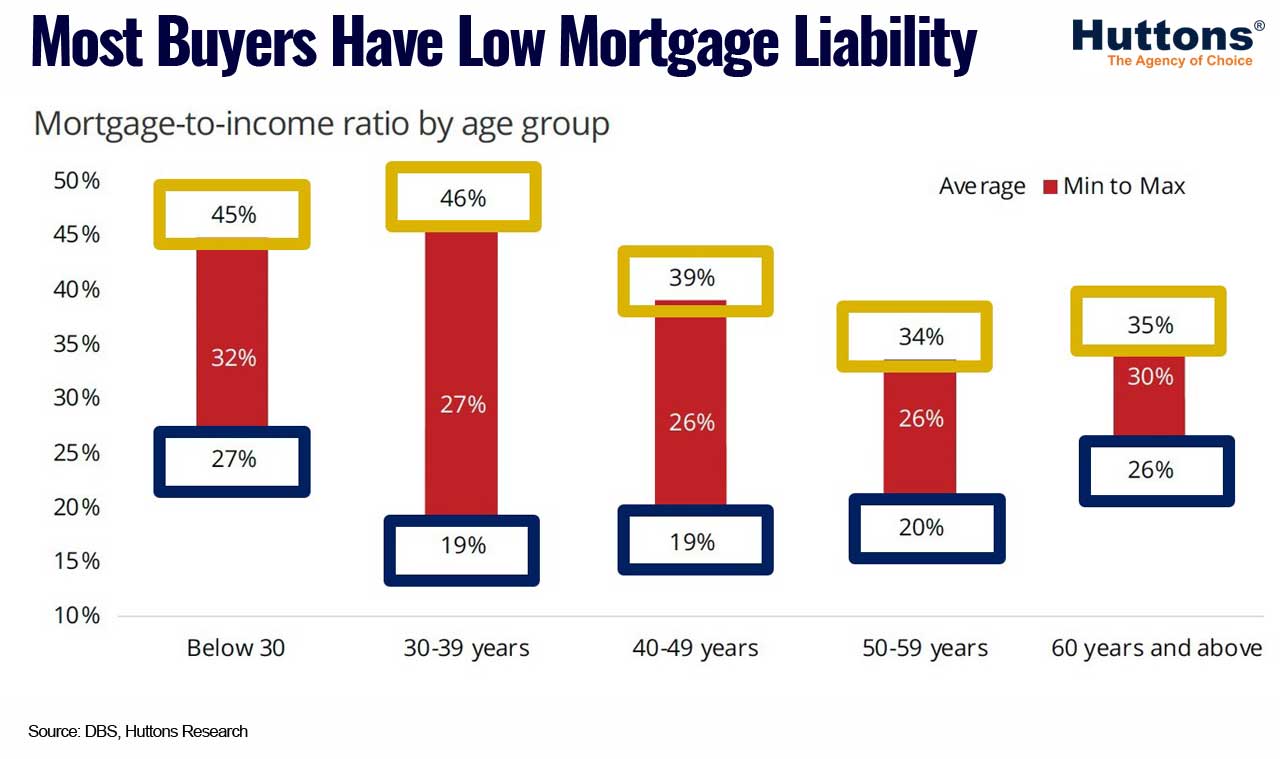

Most home buyers are generally very prudent, as reflected by the low mortgage liability.

Risen Household Income

The common perception is property prices have risen so much that they are beyond the reach of average Singaporeans.

While property prices have risen quite a fair bit, you may be surprised that household incomes have grown even faster. This means many Singaporeans can still afford to buy property, including investment property. Contrary to common beliefs, Singaporeans constitute the majority of the property buyers, including high-end properties.

Impact of ABSD in the Past

Historically, we see the impact of ABSD on property prices to be only temporary.

Singaporeans do not have to pay ABSD for their first property, and Singapore PR only have to pay a small percentage of ABSD.

Many investors are savvy enough to find ways to avoid (not evade) paying ABSD when buying their investment properties, such as decoupling and buying under trust. Hence, with the current changes, most buyers are not affected.

The private property market is driven largely by HDB upgraders. Many HDB owners ride on their highly-profitable BTO flats and Executive Condos (EC) to upgrade to private condos and even landed properties after meeting their five-year Minimum Occupation Period (MOP). With proper planning, they do not have to pay ABSD.

Will Foreigners Continue To Buy With The Increase In ABSD?

While ABSD remains the same for local and PR buyers for their first property, foreigners will now have to pay 30% ABSD even on their first purchase, up from their previous 20%.

20% to 30% is a big hike.

Will that be enough to deter foreigners from buying Singapore properties? It may take a while to get over this huge tax increase.

At this point of writing, it is reported that Hong Kong-listed Shun Tak Holdings is walking away from the en-bloc deal for High Point condominium, which it has secured for $556.7m on December 9, 2021. Has the developer lost confidence that high-end foreigners will shun away from this luxury project?

Looking from a broader perspective, Singapore property prices are still relatively low globally, which remains attractive to foreigners. Property prices across the globe have sky-rocketed, with Singapore clocking one of the weakest gains (8%) in comparison.

Our political stability and safe environment are other factors that draw foreign investors to our shore. The well-heeled foreign buyers probably won’t blink their eyes when paying the 30% ABSD. The undisputed most expensive apartment in Asia is The Peak in Hong Kong. The same buyer bought two units recently. One of them, 4544sf in size, cost HK$640 million (S$111.3 million) or S$24,493psf, which is about five times as much as our Orchard properties. The 15% tax incurred was a whopping HK$95.97m (S$16.69m)!

Increase In ABSD Will Likely Affect En Bloc Sales

The change in ABSD rates will affect developers the most, increasing from 25% to 35%.

Though developers do not pay this tax upfront, they would be liable if they do not sell every unit within five years of acquiring the land.

Because of the risk of higher ABSD, developers will exercise more caution when bidding for Government Land Sales (GLS) or going for en bloc sales. So condos going for en bloc sales will have to lower their price expectations.

Mega sites like Mandarin Gardens and Pine Grove will face more challenges because of their high price tags, which translates to higher risk.

En bloc sales in premium District 09 areas, which depend primarily on foreign buyers, may also take a back seat till developers have a clearer sense of this market segment.

Shortage of Supplies

The Covid-19 pandemic in the last two years ironically has resulted in a shortage of home supplies.

Developers have not acquired many lands because they were more concerned about clearing their high inventory to avoid incurring ABSD.

There were very few Government Land Sales, mainly because many building projects, including public housings, were delayed due to a labour and material shortage.

It creates a rippling effect. Singaporeans who want to buy BTO flats are put off by the long waiting time. So they turn to either resale HDB flats or private condos. The increased demand drives up resale prices. HDB sellers ride on the attractive resale prices to upgrade to private condos. With work-from-home and home-based-study becoming a new norm, more are looking for bigger homes. The resulted supply crunch caused demands and prices to sky-rocket across all segments.

The current inventory of new homes is hovering at an all-time low of 15,000, compared with the high of 37,000 in 2019. This acute shortage explains why we saw a new wave of en bloc fever and high bidding prices for Government Land Sales (GLS) this year.

Right after announcing the new cooling measures on December 15, the following day government said that they would release five Confirmed List sites and eight Reserve List sites for the first half of 2022 (1H2022), potentially yielding about 6,500 private residential units. More public housings will also roll out.

Do take note 6,500 new homes will not be sufficient to meet the annual demand for about 10,000 new homes. There is a chance developers may still bid a high price for the released sites simply because they are land-hungry.

I foresee prices holding up in short to medium terms as long as we face a supply crunch. Home buyers will likely return with a vengeance after the dust settles down in the next few months.

Feel free to drop me a note for a non-obligatory discussion or book me via the Calendly below for a virtual meeting if you are wondering if now is still a good time to buy a property.

Danny Han is a licensed property agent since 2005.

As a kampong (village) boy growing up in Holland Village, he has so many fond memories. He grew up with pigsty (yuk!), cemetery, swamp and communal-living (with 10 families under one roof). His childhood games were gasing (spinning top), marbles, kites, spider-fighting and tree-climbing. An open-air cinema was his source of entertainment. 7th-month Hungry Ghost wayang (Chinese opera) and getai (concert) was a once-a-year event that brought the entire village together.

What Danny is passionate about is not just about showing clients properties around Holland Village, but also enjoys sharing anecdotes and nuggets of information that are part of his growing up years.

Danny is an avid hiker and passionate foodie. He has covered most of the nature trails in Singapore, including some that are off the beaten track. Living up to his motto, “walk to eat,” he enjoys going out with his wife, a retired academician, on a food hunt across the island. He also has some foodie kakis who mix work with food. They then share their gastronomic experiences through food blogs. So do watch out, because every time he shows you a property, he will tell you what is the best food nearby!

Subscribe to receive updated practical property investment insights, property reports and good investment deals

Leave a Reply